Over the next several years, key trends will continue to emerge that should be accounted for in every hospital’s strategic planning process. COVID-19 has fast-tracked many of these factors, ultimately accelerating the healthcare industry’s transformation. At a high level, the strategy team at Octave Leadership Advisory Services is seeing:

- The healthcare industry of the future will be fundamentally different in how it is organized, how and where care is delivered, and how it is funded. While models are continuing to emerge, it is clear healthcare will be delivered in different locations, through different models, and paid for differently than we have traditionally seen

- There will likely be continued transition in hospital, non-hospital outpatient and virtual points of care. Hospitals will likely continue to see higher levels of acuity and be more specialized in their focus.

- Performance in a value-based environment will require increased focus on building continuum-wide engagement with both providers and patients.

Technological advances will make the industry more personalized, more precise and more predictive.

4 Key Trends for Hospitals to Know in 2023

More specifically, there are four key trends for hospitals to know in 2023.

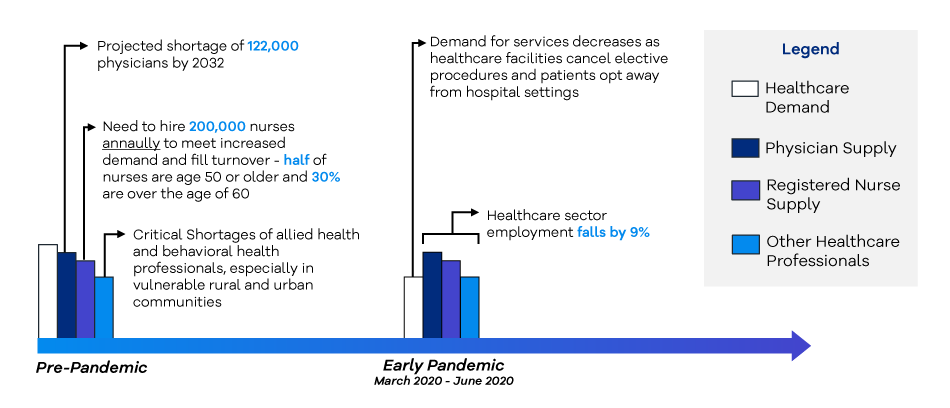

Workforce will continue to be a significant impact as we move towards the future. Around one in five healthcare workers have left their positions, creating issues with understaffing and lack of resources in hospitals and health systems. Stress, burnout and lack of balance have all been cited as reasons for staff leaving their roles.

COVID-19 has taken a heavy toll on healthcare teams who have been on the front lines of the pandemic accelerating many adverse workforce trends. Accelerated retirements, difficulty filling caregiver roles, salary escalation, and increases in traveler roles will be on-going impacts of the pandemic requiring development of innovative solutions around redesign of work.

The pandemic accelerated workforce challenges that already existed.

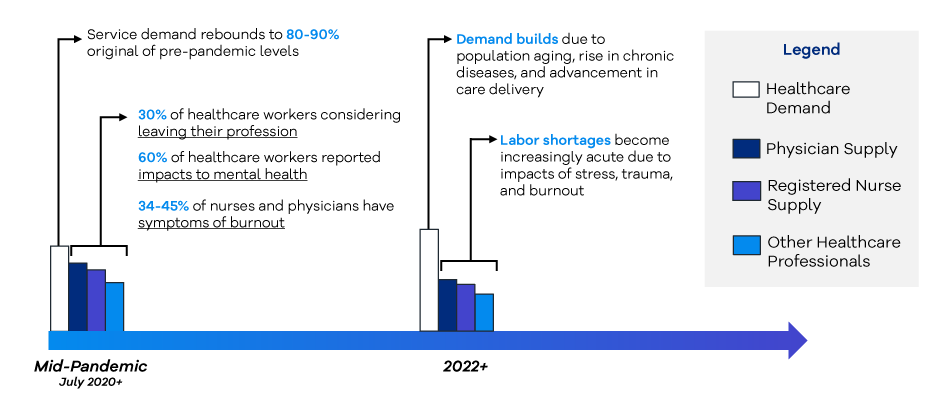

Demand has rebounded to approximately 80-90 percent of pre-pandemic levels; however, the workforce is extremely strained. Many healthcare workers are burnt out and considering employment in outside industries. As demand continues to outpace supply, we will continue to see wages increase. Ultimately, the challenge is on us as healthcare organizations to be highly thoughtful in the way we deploy services and help everyone to ‘practice at the top of license’. Additionally, it is a foundational need in our strategies to look at our workforce and determine how we are showing alignment and appreciation – particularly if we can’t ‘keep pace’ with market wages.

Patients have and will continue to seek more control over their healthcare as the financial risk is shifted to them. The pandemic has exposed patients to a universe of alternate care opportunities and, in turn, accelerated the shift to a consumer-centric operating model.

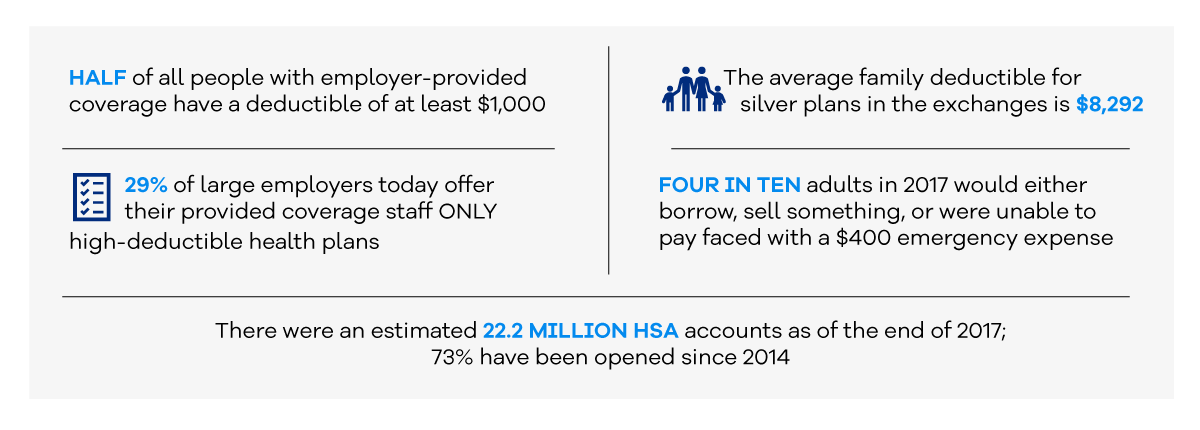

Consumerism and price sensitivity go hand-in-hand. The rise in high-deductible health plans has materially accelerated consumerism in the healthcare industry. At the same time, patients and payers are expending more energy on identifying and utilizing low-cost, high-quality access points in lieu of the traditional access points. Many employers are looking for methods to shift healthcare costs to employees to pay more out of pocket.

In the past five years, the number of workers in high deductible health plans has grown from 24 to 31 percent. In companies with 200+ workers, one third of employees are enrolled in high deductible plans. In 2020, the Kaiser Family Foundation Employer Benefits Survey determined the average general annual deductible for single coverage is $2,100+. The average aggregate deductibles for workers with family coverage are $4,500+.

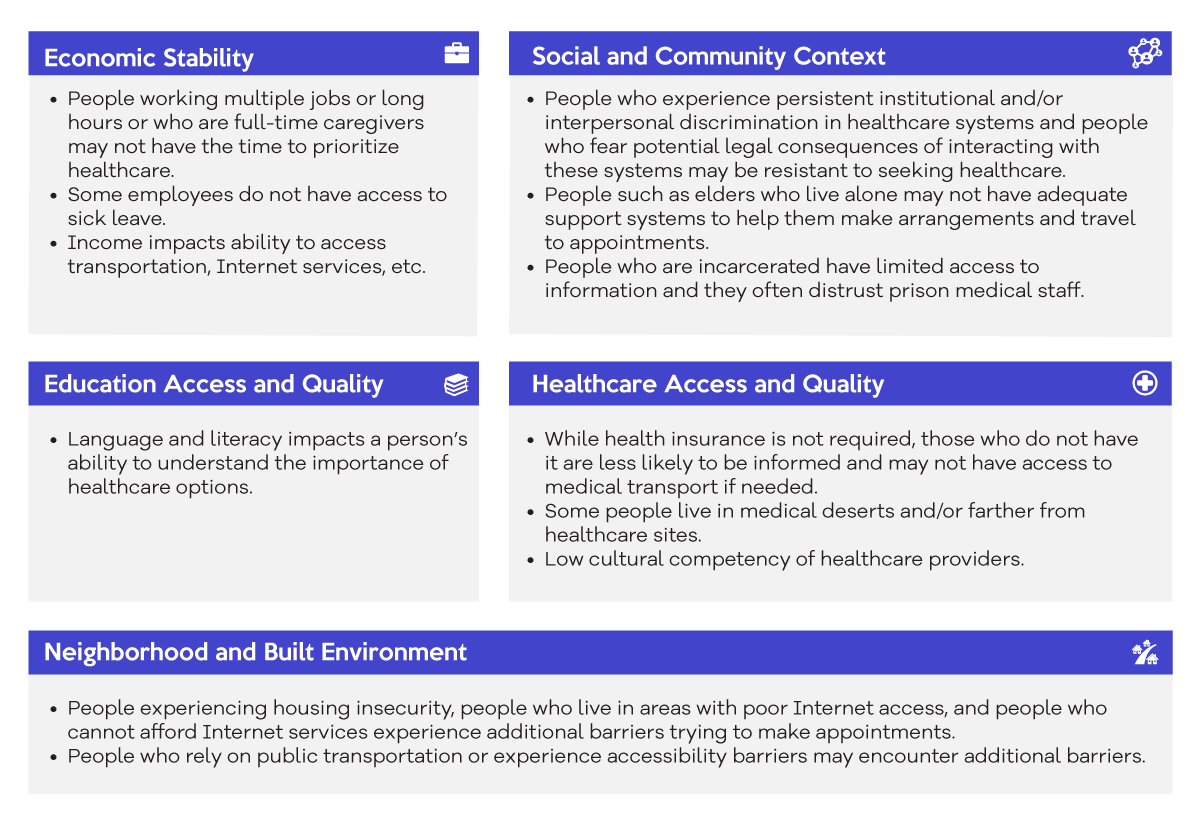

An additional emerging trend is around health equity. Health equity is achieved when every person has the opportunity to “attain his or her full health potential” and no one is “disadvantaged from achieving this potential because of social position or other socially determined circumstances.” Achieving health equity largely involves addressing social determinants of health (SDoH), many of which can be identified through a hospital’s community health needs assessment (CHNA) process.

From a strategic aspect, each of the elements above – economic stability, education access and quality, neighborhood and built environment, social and community context and healthcare access and quality – influence how and where patients receive care and can greatly impact their interactions with the healthcare system. As patients increasingly become consumer oriented, it is incumbent on us as hospitals and health systems to effectively respond and deploy services in ways that aligns to those needs.

Hospitals and health systems across the country are redesigning care delivery to improve quality and outcomes, enhance the patient experience, reduce costs and ultimately, produce better population health. They are testing and implementing new care models to focus on prevention and better coordinate care across the many sites of care that touch patients.

Telehealth continues to emerge and reshape the way patients are consuming services. For many patients, the availability of telehealth is now an expectation with 40 percent reporting they will continue to use the modality moving forward. Many physicians are also reporting they would prefer to continue offering virtual care.

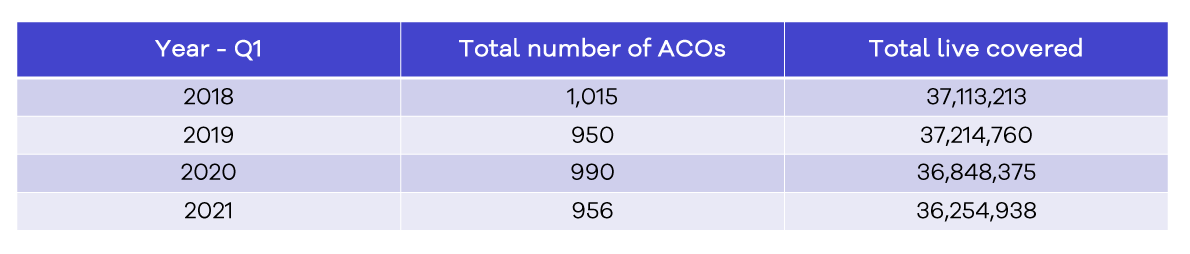

Accountable care organizations (ACOs) continue to be a force in reshaping patient journeys and containing healthcare spend. The pandemic has pushed out some lower performing ACOs; however, the number of people enrolled remains high and insurers are renewing their push for value-based care.

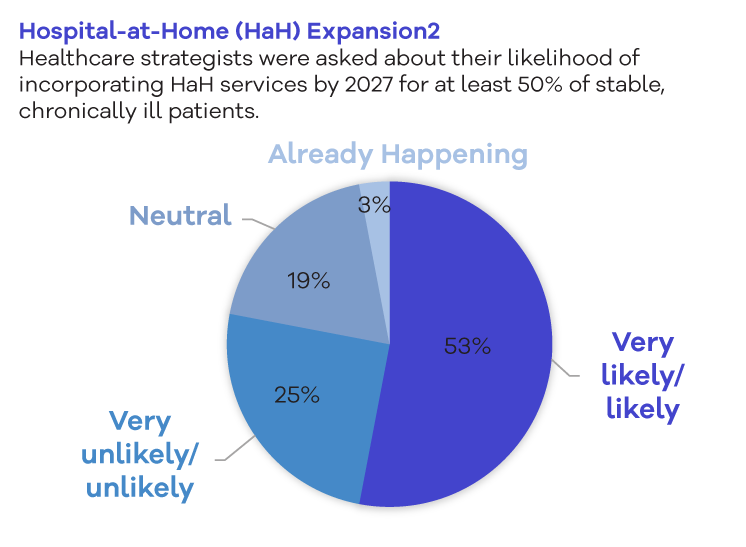

Hospital–at–home also continues to be a future growth opportunity with more than 50 percent of healthcare leaders reporting that they will incorporate those services by 2027.

Ultimately, hospitals want to ensure they are accounting for these emerging trends and participating where appropriate. Many of these offerings are too large for one organization to offer on their own but may offer unique partnership opportunities.

Big tech and retail giants have continued their push into healthcare. Existing and new competitors are deploying models as organizations seek to diversify revenue streams and capture a greater ‘share of wallet’. Traditional health system horizontal integration activity continues as providers rationalize duplicative service portfolios, attempt to scale operations, and preserve margin. However, new entrants are attempting to disrupt the industry by disintermediating patient access channels, cherry-picking high-margin services, and vertically integrating.

The pandemic also encouraged big corporations outside the healthcare sector to hire Chief Medical Officers to make sense of public health regulations and aid in containing healthcare spend.