It’s a laudable – and immensely challenging – job to run an independent hospital.

Hospitals and health systems are experiencing the worst margins since the beginning of the pandemic, putting 2022 on track to be the worst financial year for the sector since the crisis first started. More than half of hospitals (53 percent) are projected to have negative margins through 2022. Under a pessimistic scenario, Kaufman Hall estimates 68 percent of hospitals will have negative margins this year.

What’s driving negative margins – increasing expenses for labor, supply, purchased services, drugs and more plus decreasing inpatient volumes, utilization of revenue resources and reimbursement – is highly likely to persist in 2023. That means it will be just as difficult to manage an independent hospital in 2023.

That’s why I’m strongly encouraging the boards of directors and C-level leaders of independent hospitals to consider the guidance below and get ready.

Complete Annual Strategic Plans and Review Quarterly

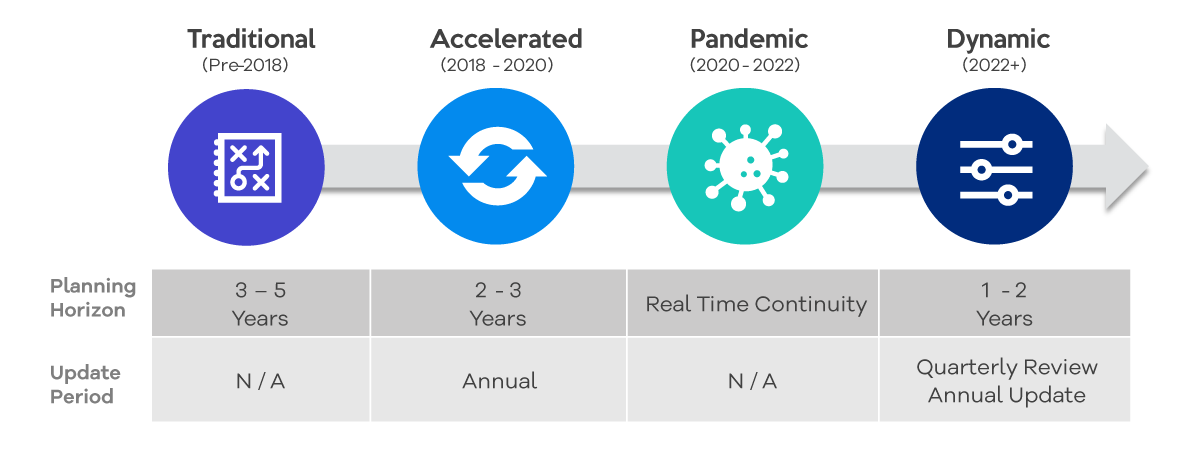

Updating strategic plans on a regular basis and around significant changes in the operating environment has long been a best practice. Traditionally, healthcare strategic plans have examined a period of between three to five years. In certain circumstances, organizations may have even engaged in strategic and long-range planning for periods of 10+ years.

However, the pace of change experienced in recent years has accelerated the cadence for review and updating of strategic planning and forecasting documents. As the hospital industry has emerged from the COVID-19 pandemic, planning cycles have become far more dynamic, requiring frequent review, update and contingency planning.

A solid strategic planning process includes data from:

- The latest community health needs assessment (CHNA),

- Comprehensive service line data about market share, leakage, yield under existing contracts and operating financials,

- Qualitative data from key stakeholder interviews: patients, employers and businesses in the community.

The most effective hospitals bring a comprehensive understanding of the market and regulatory forces, the payer environment, patient and employer community needs and wants, their individual situation, comparator performance, and current and emerging competitive threats to their strategic planning process as well as quarterly updates to the strategic, financial and operational plans.

Collaborate and Explore Unique Partnerships to Create “Systemness”

Very few hospitals can continue to have a go it alone attitude and succeed. I have previously written about the downsides of hospital mergers – higher prices, a reduction in patient, maternal and neonatal, and surgical services, and physician burnout.

That’s why some highly effective hospitals have chosen to collaborate and gain leverage and economies of scale, while still maintaining the independence that makes them vital to their communities. One example from our work at Octave Leadership Advisory Services is two hospitals that often competed for patients and resources in the past. Today, those hospitals are utilizing Octave’s shared services and imagining the delivery of patient care and the distribution of services differently. They are identifying and prioritizing the key areas of critical importance to their success, an ongoing collaborative process. It’s been gratifying to see Octave’s leaders work with the hospital leaders to build a different health system.

Other ways to collaborate are:

- Leverage shared services for specialized functions such as revenue cycle, payer contracting, technology and cybersecurity, group purchasing and operations,

- Access fractional FTEs for specialty and subspecialties and

- Form affiliations that keep local control, where shared governance or management might be in place, but services and decision-making still rest with the local community and boards.

Prioritize Culture to Help Mitigate Workforce Challenges

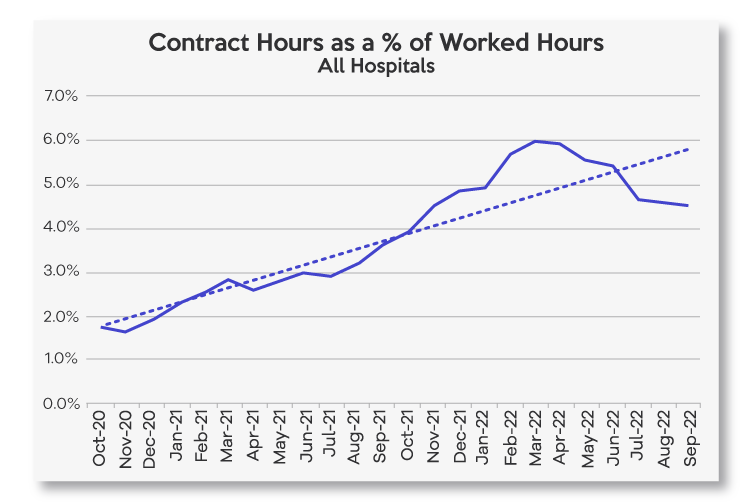

There is some evidence that the use of temporary staff and travel nurses is beginning to revert to pre-COVID-19 levels. In 2022, contract and agency hours as a percent of total hours has increased 126 percent in 2022 versus 2020 and 2021 but has been trending down in the last few months.

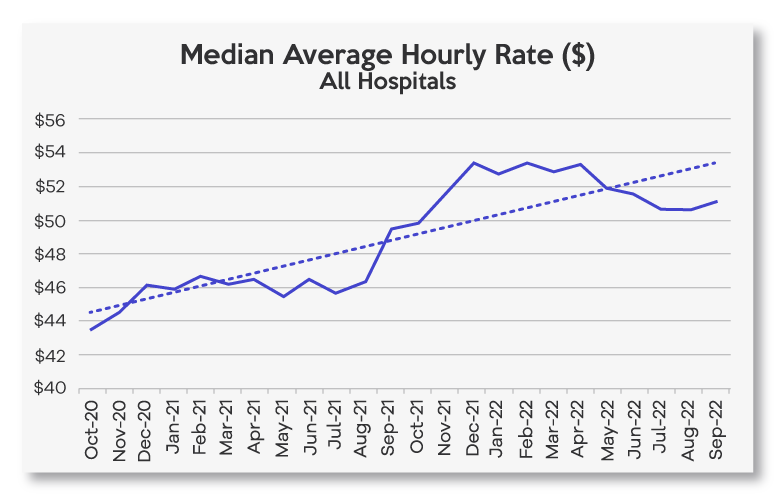

Nevertheless, in 2022, average wage rates at hospitals are up 16 percent compared to 2020 and 2021[1] and workforce will continue to be a top challenge as independent hospitals increasingly compete with Walmart and Publix for entry-level and lower-level employees.

We recommend independent hospitals identify and replicate the things that make hospitals and health systems like Wooster Community Hospital an employer of choice in their community. For Millennial employees who tend to prefer meaningful work experiences, connecting all roles at a hospital to the organization’s mission will help with recruiting. Hospitals are also advised to use exit interviews to determine the real drivers of turnover at their organizations.

A report from McKinsey & Company reports the United States may see a nursing shortage of 200,000 to 450,000 registered nurses by 2025, suggesting the national shortage of nurses will continue indefinitely. That means independent hospitals are advised to create partnerships to feed their nursing pipeline. For example, members of Octave’s Chief Nursing Council are:

- Strengthening connections with nursing schools by hiring and paying students while they are doing their clinical hours and recruiting new nurses before they graduate,

- Repaying nursing school costs and supporting licensed practical nurses (LPNs) who are pursuing registered nurse (RN) degrees and

- Creating volunteer programs for interested high school students.

Leverage Price Transparency Data

On July 1, 2022, national, regional and local payers released full contract rate information in machine-readable files. Given the file sizes, field variances, type variances and the like, a high degree of sophistication is needed to download, compile and analyze the files across carriers.

That’s why organizations like Sage Transparency and Turquoise Health are aggregating pricing data and disclosing the average rate by payer and clinical category at the hospital, health system and state level, averaged by service and rate type. Turquoise Health lists average rates for inpatient facility, outpatient facility, physician and outpatient facility plus physician rates for four payer classes: commercial, Medicaid, Medicare and cash.

Commonly, for independent and rural hospitals, reimbursement terms are handed down from payers and there is little opportunity to impactfully negotiate. Instead, armed with robust pricing data, hospitals and health systems can negotiate better payer reimbursement rates.

Create and Hone Your Outpatient Strategy

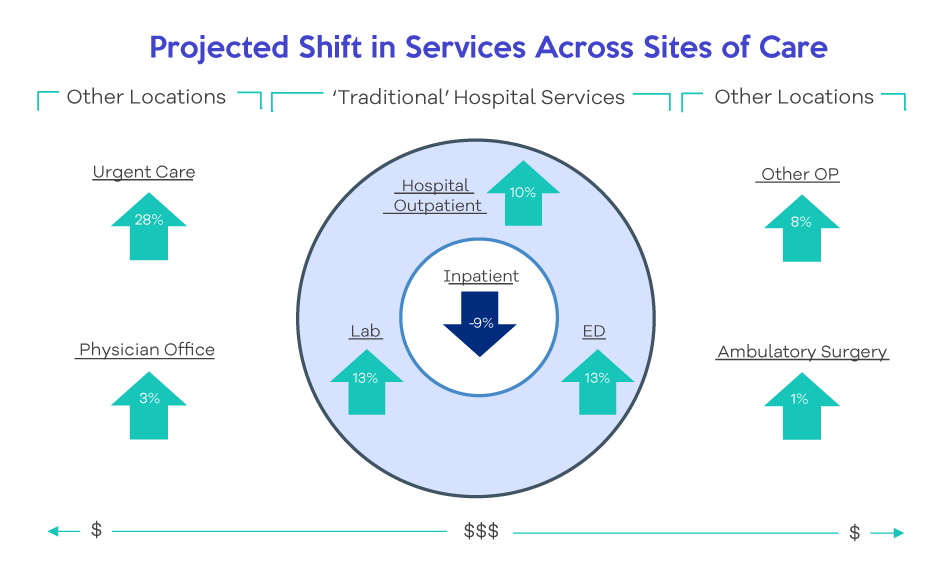

In 2022, inpatient hospital volumes have decreased as alternative sites of service have grown. As services shift away from the inpatient arena, they are moving into less acute settings across the care continuum such as urgent care and ambulatory surgery centers (ASCs). Payers are continuing to move services to outpatient/ambulatory and lower acuity settings, which means this trend is likely to continue for the foreseeable future.

Community-based hospitals have the opportunity to capture or recapture volume as patients are generally less inclined to travel for lower acuity, ambulatory-based services. To facilitate this growth, health systems must work to create appropriate physical and virtual access points to satisfy consumer needs.

Become a Convenor of Resources

Rather than taking exclusive financial responsibility or directly providing all of the services needed by a community, hospitals have the opportunity to become a convenor of resources. Hospitals can be a vital convener in coordinating and partnering with other community organizations, forging community relationships and establishing new partnerships with the aim of improving population health and community vitality.

[1] Certain data used in this study were supplied by Syntellis Performance Solutions, LLC (“Syntellis”). Any analyses, recommendations or advice based on these data are solely that of the author(s) and not Syntellis.