Octave Advisory Services Leadership 2022 Conference in the hope of providing some insight that can be assistive, and out of appreciation for all independent hospitals. I am deeply concerned about the fragility of community-level care, the further tumult caused by the COVID-19 pandemic and the spiraling impact it has had on patient and caregiver satisfaction as well as burnout.

There are a number of current market conditions and trends that challenge the future of community hospitals, including:

- The consolidating healthcare market,

- The sustainability of rural hospitals,

- Patient outmigration,

- Commercial payer negotiations,

- Government programs, and

- Employers

The Consolidating Healthcare Market

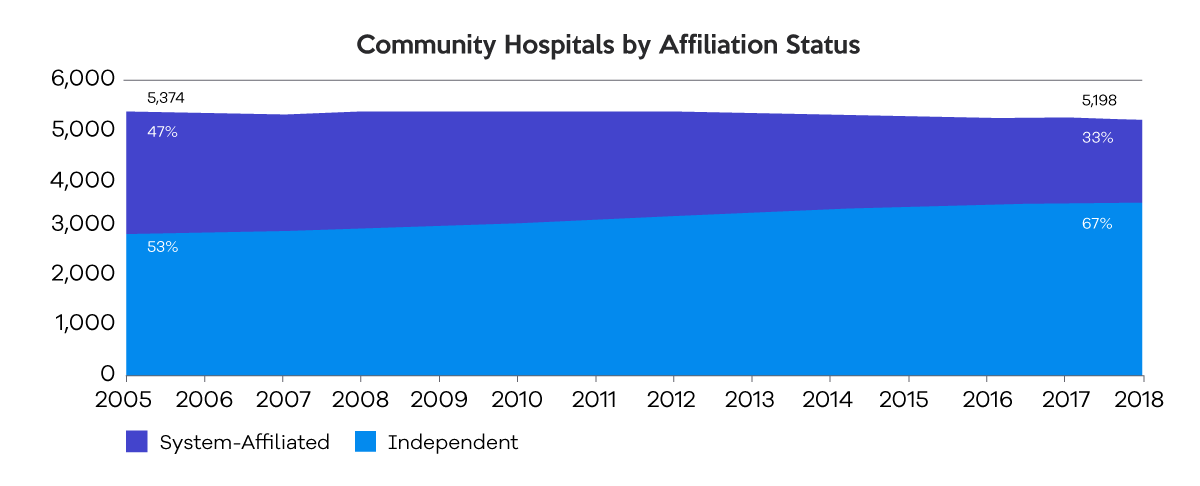

Market consolidation has decreased the number of independent, community hospitals, and raised the number of those forming an affiliation with another hospital or a health system. From 2005 – 2018, the number of independent community hospitals decreased by 33 percent, while the number of system-affiliated community hospitals rose by 23 percent.

With margin erosion and ever-increasing sophistication in technology, process and medical technique, specialty and subspecialty, the chasm between the hospital haves and have nots has widened. As going it alone has been increasingly more difficult, far too many community hospitals have come to believe the solution is to either close or merge.

Hospital acquisitions, by the numbers:

Hospital mergers and acquisitions have given the 10 largest healthcare systems control of a quarter of the market.

“When hospitals merge, they face less competition and charge as much as 40 to 50 percent higher prices than if they had not merged or consolidated,” according to the Federal Trade Commission’s Director of the Bureau of Economics.

As referenced in the Kaiser Family Foundation Issue Brief, What We Know About Provider Consolidation,

– In 2020, MedPAC concluded the “preponderance of evidence suggests that hospital consolidation leads to higher prices.”

– A study of the 25 metropolitan areas with the highest rates of hospital consolidation from 2010 through 2013 found the price that private health plans paid for the average hospital stay increased in most areas between 11 and 54 percent in the subsequent years.

An analysis of employer-sponsored coverage discovered hospitals without competitors in a 15-mile radius have prices that are two percent higher than hospitals in markets with four or more competitors.

What we understand from study after study is that none of the merger and acquisition activity improves quality.

The Forces Driving Hospital Consolidation

Rural Hospital Sustainability

As the CEO of Octave Leadership Advisory Services, Dr. Dwayne Gunter discussed in a recent blog, 25 percent or 354 hospitals across 40 states, representing 51,800 community employees and $8.3 billion in revenue, are at high risk of closing unless their financial situations improve. Of those hospitals at high financial risk, the authors of the Rural Hospital Sustainability Index found that 81 percent are considered highly essential to their communities.

Patient Outmigration

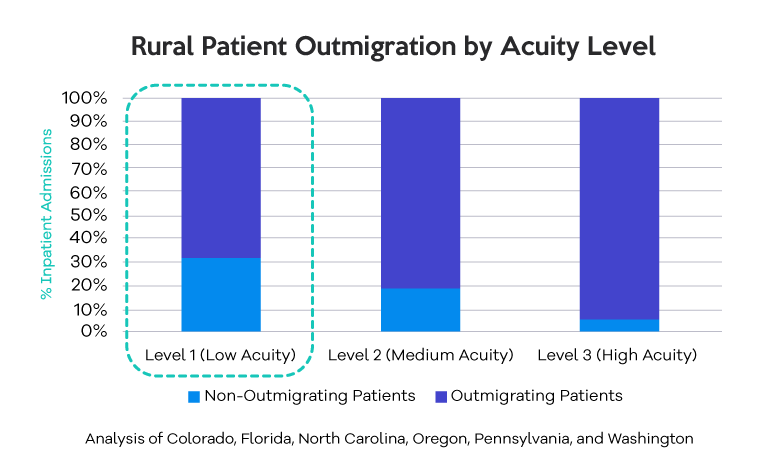

In a study of 747 hospitals in Colorado, Florida, North Carolina, Oregon, Pennsylvania and Washington, Guidehouse determined that more than three-quarters of patients living in rural counties with a local hospital out-migrated for care, even when care was available in community, as compared to 35 percent and 23 percent of suburban and urban patients.

Since some of the outmigration can be explained by a lack of higher acuity services available in the local community, Guidehouse dug into the Medicare DRGs (diagnosis-related groups) to determine that 68 percent out-migrated for low acuity conditions such as treatment for COPD, acute myocardial infarction, diabetes and minor orthopedic procedures.

Commercial Payer Negotiations

As one who has worked with health plans for much of my career, I know commercial payers understand the unique value of community hospitals. They also are aware of the inflationary pressures from hospital mergers and acquisitions. Nevertheless, their day-to-day reality dictates where they have to focus their time and energy. At any given time, a payer may have 50+ active negotiations. That means they must prioritize those deals that are most meaningful to their organization and their employer customers, in terms of overall dollar impact or the number of affected individuals. It also means reimbursement terms are often pre-set for community and rural hospitals with little opportunity for negotiation and insufficient volume to qualify for payer incentive programs.

Contemporaneously, payers continue to move more services to outpatient, ambulatory and lower acuity settings through a combination of medical policy, plan design, patient and contract incentives, and payment differentials for ambulatory care sensitive conditions (ACSCs) – ACSCs are comprised of 19 different conditions such as asthma, angina, pelvic inflammatory disease, gastroenteritis, congestive heart failure, severe ear-nose-throat (ENT) infections, epilepsy, bacterial pneumonia, tuberculosis, iron deficiency anemia in children up to 5 years of age, cellulitis and dental conditions.

It is important to note that payer fee schedule increases, inclusive of COLAs, are no longer a given. Commercial health plans are building in baseline performance measures that require hospitals and physician organizations to earn pay and fee schedule increases. These requirements span utilization, site of service and quality components.

Payers are continuing to increase pressure on risk assumption by:

- Actively targeting and sunsetting percentage of charge contracts,

- Establishing total medical expense budgets or global capitation targets for the attributed population with risk corridors, upside and downside caps, and provisions for outliers,

- Leveraging ambulatory payment classification (APC) methodology for outpatient services, and

- Utilizing episodes of care where there is sufficient volume and incentivizing patient migration to high volume centers and in-network Centers of Excellence.

Government Programs

In July, CMS proposed changes that provide further support and incentives to move into an accountable care organization (ACO) arrangement, particularly targeting rural and underserved populations. The proposed fee schedule also incorporates a statutorily required drop of $1.53 in the conversion factor, from $34.61 to $33.08, or 4.42 percent. For the quality payment program, CMS is proposing five new, optional Merit-based Incentive Payment System Value Pathways (MVPs) that would be available beginning in 2023. These MVPs align the reporting requirements of the four MIPS performance categories around specific clinical specialties, medical conditions or episodes of care. The CMS proposal also includes expanded coverage for behavioral health and substance abuse treatment as well as the Rural Emergency Hospital Designation, a rule that would allow small rural hospitals to change designation and provide emergency, observation, outpatient and capped limited overnight services.

For additional insight into the proposed 2023 CMS changes, The Learning Institute offers frequent finance and reimbursement webinars and educational events.

Employers

Having worked with employers and employer coalitions for decades, I have seen the trend only increase where hospitals go directly to employers to contract for a broad range of services, develop a narrow network benefit plan design or deliver a niche set of services focused on wellness and preventive care. Employers have always and continue to value care in the communities of their employees, but just as importantly, they want to see health cost trends mitigate. Therefore, there is a degree of openness on the part of many to collaborate. There are funding vehicles that can help facilitate this work, with reinsurance to protect hospitals, and wraparound networks to accommodate out of area care. For this to occur, a high degree of sophistication and strong access to data are essential.

Read part two of my blog to learn about the seven key disciplines of highly effective hospitals. Click here.